- Mr Market

- 6-Feb-2015

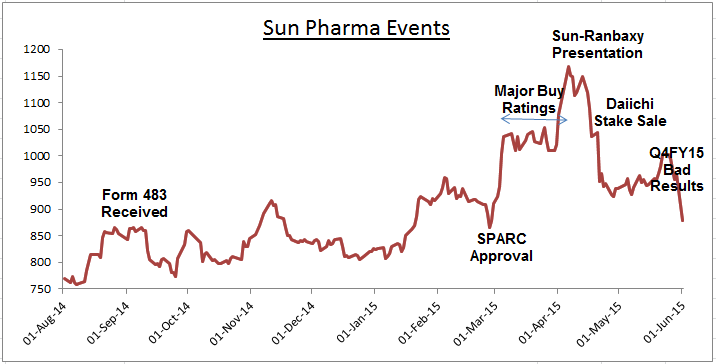

Sun Pharma is the largest Indian pharma company by market capitalization and its owner is Indias richest man. Owing to such credentials, analysts from over 38 broking houses track the company. Prior to the Q4FY15 results, 36 out of 38 analysts had either a BUY rating or a HOLD rating, indicating that the stock was expected to give 10-30% returns over the next twelve months. However, Q4FY15 results of Sun Pharma were much below the analyst expectations and the stock price declined by 9% in a single day. It lost Rs. 23,500 crores in market value in a single day! For the year, it has declined by 27% from its peak of Rs1,200, which is a substantial decline for large cap like Sun Pharma.

While there are various reasons at play, an important event happened before the Q4FY15 results - The Japanese firm Daiichi Sankyo, who sold Ranbaxy to Sun Pharma, sold its entire stake in Sun Pharma (which it got as a part of the Sun-Ranbaxy merger) through open market. The sale was valued at nearly Rs. 18,000 crores at the price of around Rs. 950 per share. The price of Sun Pharma shares before the offer was announced was Rs. 1050.

- 15-Sep-14: 483 Received for Halol.

- 04-Mar-15: SPARC Drug Approval

- 07-Apr-15: Sun Pharma - Ranbaxy Merger Presentation

- 07-Apr-15:Most Analyst Buy/Hold Ratings (Check Brokerage Radar)

- 07-Apr-15: All time high; News paper headlines.

- 20-Apr-15: Daichi Sankyo Stake Sale worth Rs. 19000 crores.

- 20-Apr-15: Stock fell by 10% before announcement and 10% after announcement.

- 29-May-15: Sun Pharma Bad Results. Missed FY15 Guidance, No Guidance for FY16, Doubts over Halol Plant.

- 01-Jun-15: Stock Falls to Rs. 875. Down 10% in a day. 25% Down from Peak.

We would like to highlight some interesting behavioral traits that manifest during such investing cycles

1. Analyst estimates cannot be taken for granted: Most analysts make future projections by forecasting the current trend. For a company operating in competitive environment, there are multiple factors that can affect the short term earnings so it is only natural that analysts are unable to capture the intermittent volatility. Some analysts may not even have a deep insight to the company’s business but may estimate the companys earnings due to pressures of their job. Depending completely on analyst estimates for your investments may not be a good idea.

2. Extreme dependence on Management Guidance: A large part of the investing / trading world depend a lot on what management has to say about the immediate future. Most questions are ultimately trying to have easy answers for the following questions:

- What is the sales growth going to be? If possible for the next year and if possible also guide for the next quarter

- What will be the margins?

- What will be the tax rate, interest, etc.

We must understand that in a world driven by uncertainty, there is a non-zero probability of management guidance not being achieved. Investors must try and form their own assessment and view the management guidance in that context.

3. Large Caps Not SAFE at ANY price: Investors often attribute safety as one of the advantages of investing in blue chips or large cap stocks. However, we just witnessed the case of a blue chip falling by 25% in less than a month. Sun Pharma might be the best pharma company and its stock may give good returns in the very long term, but short term is very unpredictable. Investors wanting to have an exposure to equities have to accept volatility in the short term.